FIRE Travels Well — But Does It Translate?

Retire at 40. Live off your investments. Never work again. Sounds like the dream, right? The FIRE movement has convinced thousands of Indians that this is not just possible — it is a plan. And it is easy to see why the idea is spreading here — rising salaries, a booming market, and a generation tired of the 9-to-5 grind. It has traveled well — from American personal finance blogs to Indian Twitter threads to dinner table conversations. But the movement was designed for a very different country, with a very different safety net. So before we adopt this idea, it is worth asking: what exactly are we importing?

America Built the Runwa

The American retiree, even one who exits the workforce at 40, is not entirely on their own. Social Security provides a baseline income that kicks in later in life. Medicare covers healthcare from age 65. These are not trivial supports. They fundamentally reduce the size of the corpus an American needs to accumulate, because the government eventually picks up two of the highest costs in retirement.

Layer on top of that a higher per capita income, access to low-cost index funds, and decades of compounding equity returns, and the mathematics of FIRE begins to make sense. The famous 4 percent withdrawal rule (according to this rule, you can withdraw only 4% from your retirement corpus each year, adjusted for inflation) — the bedrock of most FIRE calculations — was derived entirely from American market data. It reflects American realities. For a disciplined, high-earning American professional, FIRE is genuinely achievable. The system was, in many ways, designed to make it possible.

But India’s A Different Airport

Now bring that same framework to India, and several things start to break down.

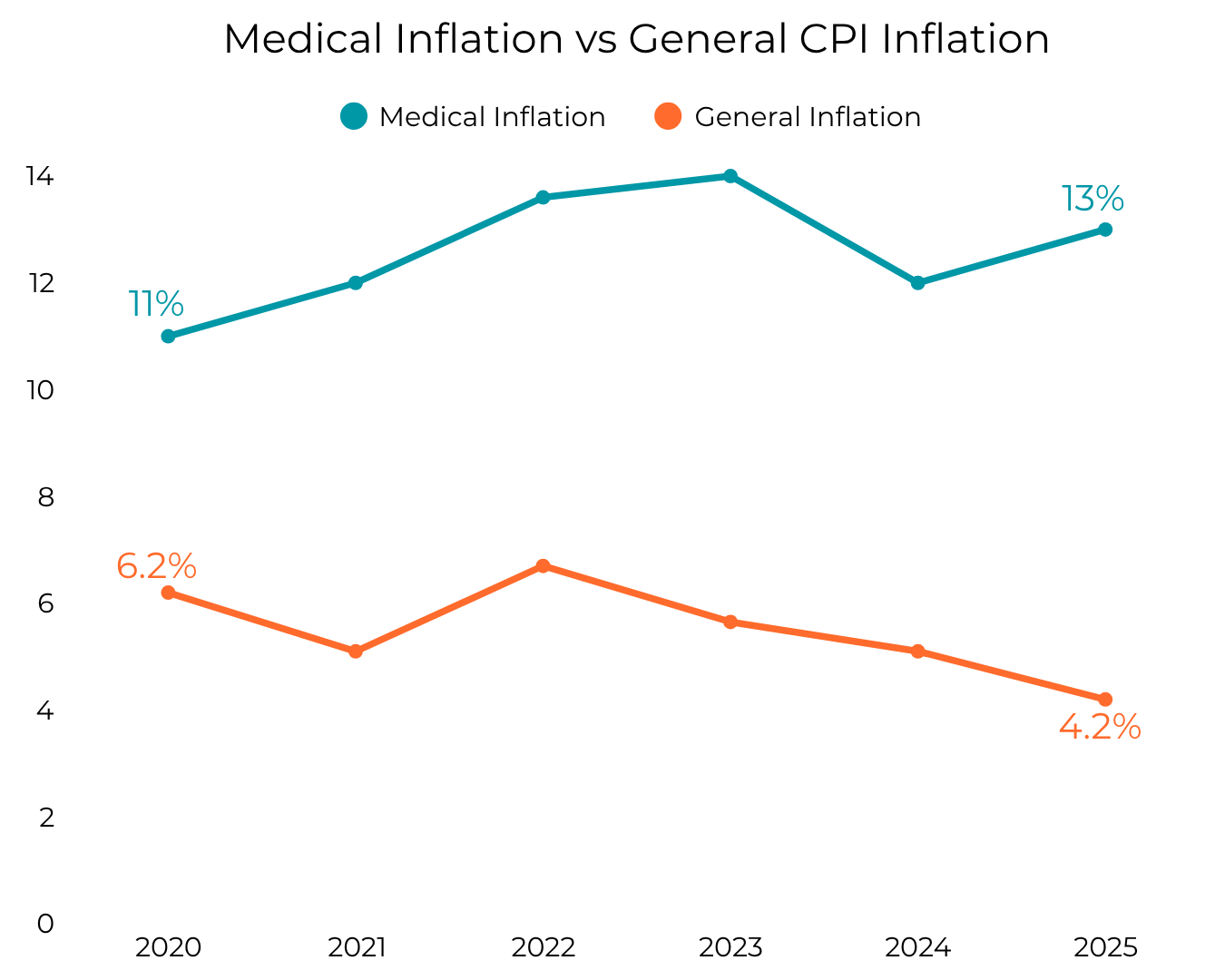

There is no social security net. No universal healthcare. If you retire at 40 and face a serious health crisis at 55, the entire financial burden falls on your personal savings — and healthcare inflation in India has been running at 12 to 14 percent annually. That is not a rounding error. That is a portfolio-destroying number if you have not planned for it specifically.

Then there is the family dimension. Indian financial planning has never been purely personal. Aging parents, children’s education, weddings, and family obligations create demands on a corpus that Western FIRE literature simply does not account for. An Indian planning for early retirement is not just planning for themselves. They are planning for several people around them — often without knowing exactly when or how much those obligations will arrive.

Longevity adds yet another layer. Someone retiring at 40 in India today may need their savings to last 50 years or more. Running a 4 percent withdrawal rate over half a century, through Indian inflationary conditions and without a government backstop, is a considerably more precarious calculation than the same math done in an American context.

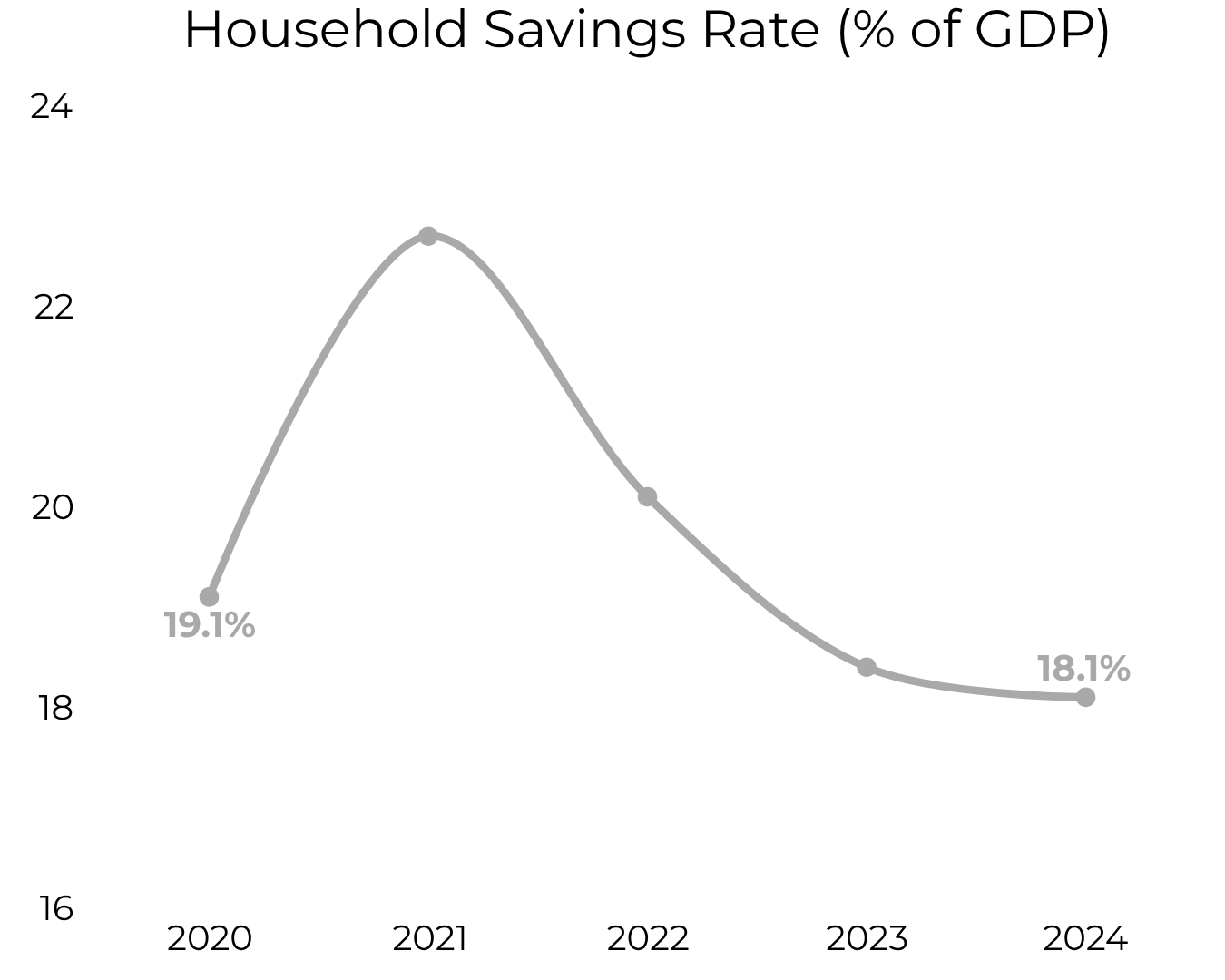

And honestly, the income reality matters too. The proportion of Indians who can genuinely save 50 to 70 percent of their income — after taxes, after family obligations, after the cost of living in Mumbai or Bengaluru — is very small. FIRE, as currently conceived, is a conversation available to a narrow slice of high-earning professionals.

So Let’s Chart a Different Flight Path

The spirit of FIRE — building financial independence, reducing dependence on a single income stream, having enough to make choices freely — is deeply worth pursuing in India too. The goal is right. The execution needs recalibration.

An honest Indian version would treat healthcare as a separate, inflationary cost with its own dedicated corpus. It would build in explicit buffers for family obligations rather than hoping they average out. It would stress-test withdrawal rates against Indian inflation, not American historical data. And it would probably define the finish line not as stopping work entirely, but as reaching a point where work becomes a choice rather than a compulsion.

That last part might actually be more meaningful than quitting at 40 ever could be.

The FIRE movement asks the right question — how much is enough, and when can you stop? India deserves to ask that question too. It just needs its own set of answers