Why Cycles Matter in an Investing Framework

Why Cycles Matter in an Investing Framework

Investing would be a lot simpler if one strategy worked all the time. Buy quality businesses, hold forever, collect returns. Sounds clean. The problem is that markets do not work that way, and the sooner an investor internalises that, the better their decisions tend to be.

Every asset class — equities, fixed income, real estate, gold — has a moment. And within equities, every investing style has its season. There are stretches where quality and moats dominate. There are periods where pure growth, even without earnings, runs ahead of everything else. There are years where value investing looks foolish right until it doesn’t. The investor who mistakes one season for a permanent climate tends to be badly hurt when the weather changes.

This is what makes cycle awareness so central to investing. It is not about timing the market perfectly — that is a fool’s errand. It is about knowing, broadly, where you are and adjusting your strategy accordingly. Getting that read right does not guarantee returns. Getting it wrong, however, almost always costs you.

The Lesson 2007 Left Behind

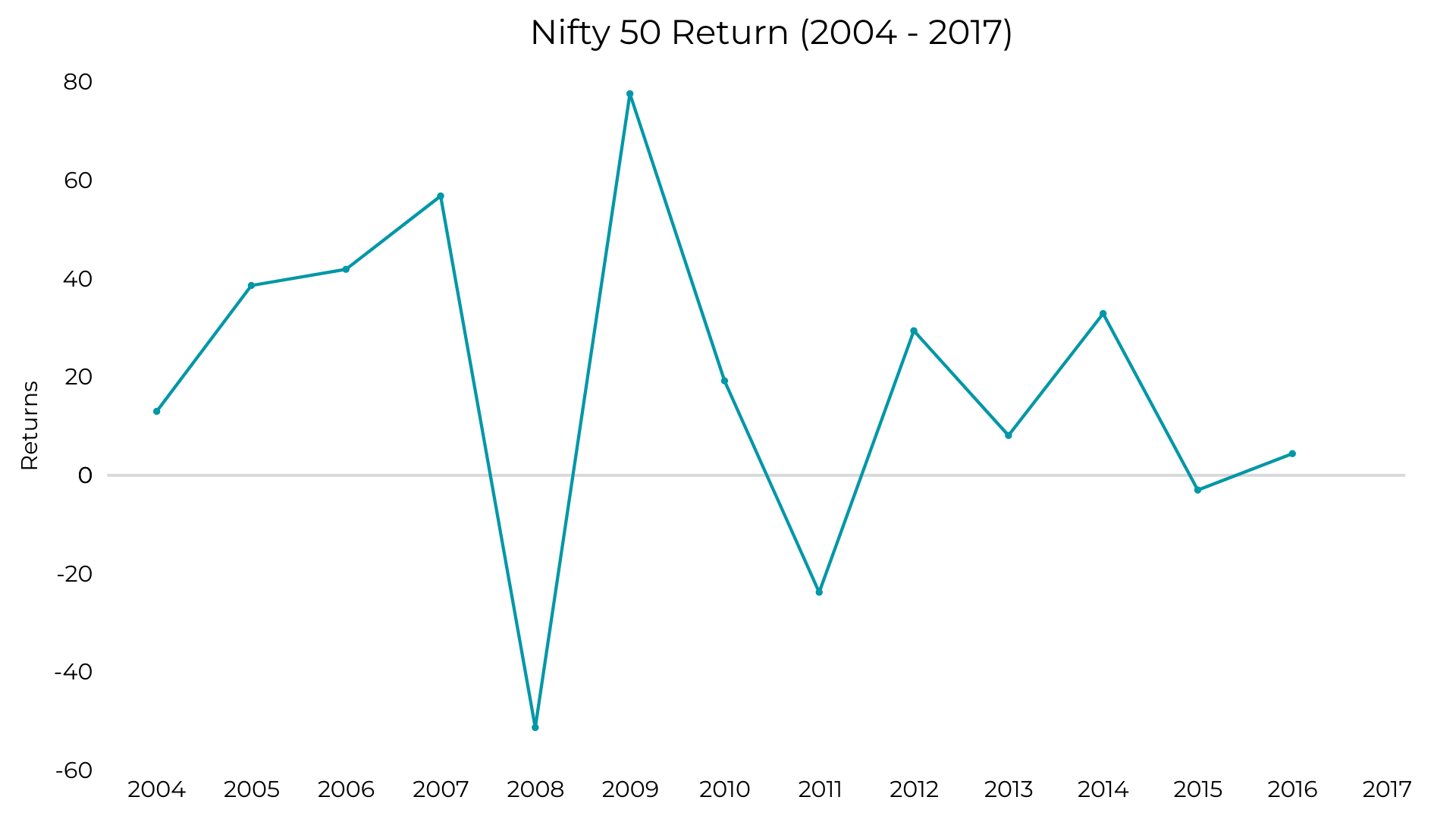

Look at what happened in the years leading up to 2007. Infrastructure was the story. Companies without particularly strong fundamentals were being re-rated simply because they were in the right sector at the right time. Meanwhile, businesses with genuine competitive advantages — the kind that compound quietly over the years — were being ignored. Quality without a near-term catalyst was unfashionable. Growth without quality delivered decent returns between 2004 and 2007 simply because the tide was rising and lifting everything with it.

Then the tide went out.

Post 2007, the narrative flipped entirely. Moat-based investing — owning businesses with durable competitive advantages, strong balance sheets, and real pricing power — outperformed for the better part of six to seven years. The very companies overlooked during the infrastructure frenzy became the market’s darlings. Pharma, consumption, quality franchises — sectors that had significant margins of safety in 2007 but were ignored because commodities and capital expenditure stories were stealing all the attention.

The cycle had turned. Those who recognised it early were rewarded. Those who stayed anchored to what had worked before spent years wondering why their portfolios were going nowhere.

What is worth noting is that in 2007, few people saw a connection between retailing and technology. They seemed like entirely separate worlds. That assumption turned out to be deeply wrong. Today, retailing is almost entirely dependent on technology. The moat that physical retail once had did not just weaken — it collapsed. And the investors who did not track changes in the underlying environment missed the signal entirely.

Moats Are Not Forever

This brings up one of the more uncomfortable truths in investing. Moats — those durable competitive advantages that justify premium valuations — are not permanent. They erode. Sometimes slowly, sometimes with alarming speed.

Walmart met every standard test of moat investing. Then Amazon came along, and the advantage that had taken decades to build started to look far more fragile. Print media had a moat — high barriers to entry, loyal readership, and pricing power with advertisers. Technology dissolved it within a generation. In India, large IT services companies held an almost unquestioned moat as recently as 2015. A combination of digital disruption and shifting client expectations has significantly eroded it since.

This is precisely why investing cannot be reduced to a formula. The moment you systematise it completely, you stop asking whether the conditions that made the formula work still exist. Every cycle rewards a different set of assumptions. The assumptions that drove returns for six years post-2007 are not the same ones that will drive the next six.

Being Early Looks Wrong Before It Looks Right

Here is the part that tests most investors. Correctly identifying a cycle shift and positioning for it does not feel good immediately. The market will disagree with you for longer than seems reasonable. The strategy that worked last cycle will keep working just long enough to make you doubt your own read.

The investors who stayed anchored to quality and valuation discipline through 2004 to 2007 navigated 2008 with far less damage. And those who had the conviction to buy when everything looked broken were the ones who compounded the most in the years that followed. That kind of discipline requires a framework built around cycle awareness — not a rigid formula, but a flexible understanding of where different strategies tend to outperform and why.

No single approach works across all environments. The investor’s job is not to find the one strategy that works forever. It is to understand which approach fits the current environment and have the patience to stay with it long enough for the cycle to play out. Cycles do not announce themselves — they are only obvious in hindsight. Which is exactly why a framework that respects them is the more durable, and ultimately more rewarding, way to invest.