Will SIF Find Its Place in the Indian Investor’s Portfolio?

Will SIF Find Its Path — Just Like Mutual Funds Once Did?

Cast your mind back to the early days of Indian mutual funds. UTI launched in 1964, but for decades the category remained largely invisible to the average investor. Returns were modest, awareness was low, and the few who did invest barely understood what they owned. By the 1990s, mutual funds were still a niche. It took SIPs, SEBI’s investor education push, and a whole generation of financial advisors to turn them into the ₹60+ lakh crore industry they are today.

Specialised Investment Funds are now at roughly that same stage — only a few months old and largely untested. The question worth asking is not whether SIFs are perfect today. The real question is: does the category deserve time to grow into itself?

What SIFs actually are

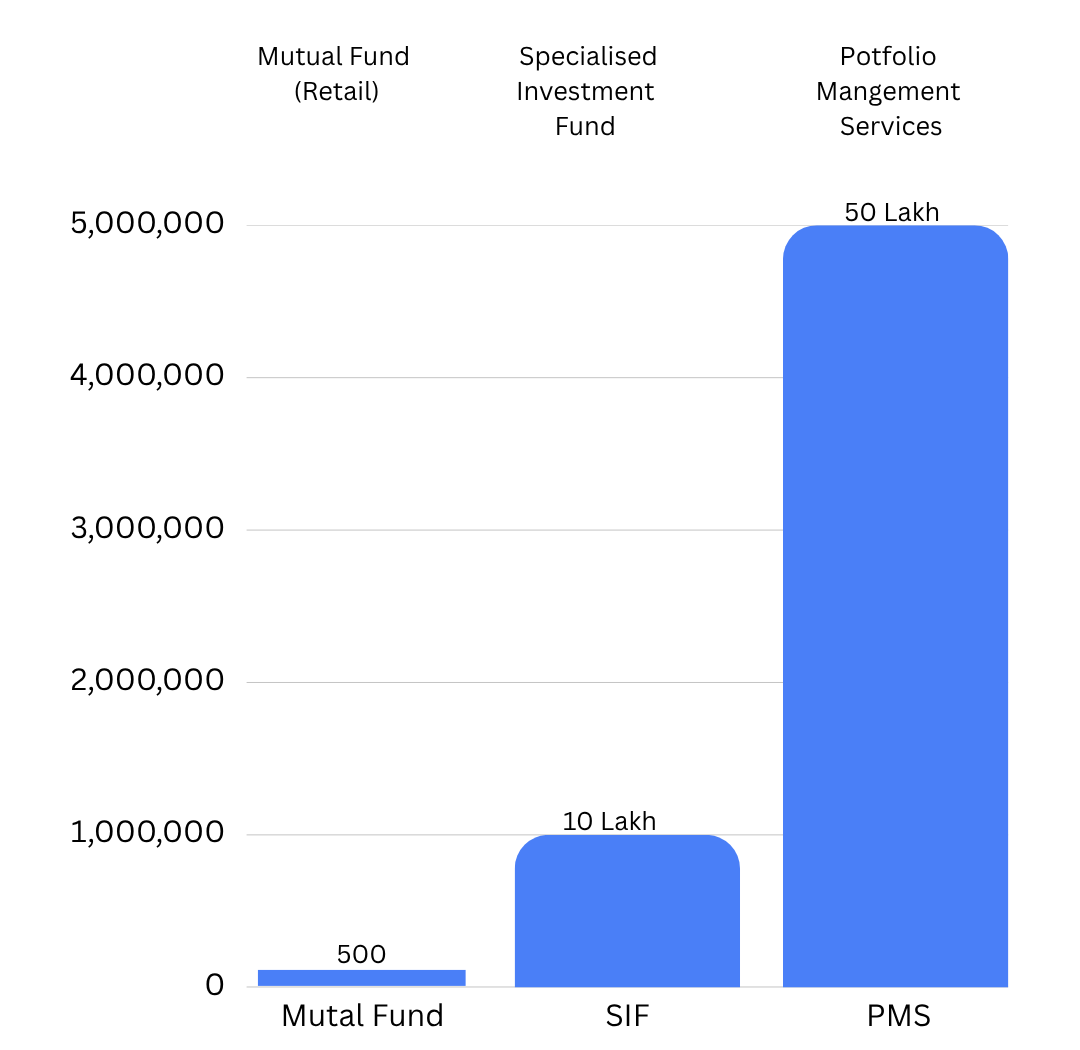

Introduced by SEBI in December 2024 and live from April 1, 2025, SIFs were built to fill a genuine gap. On one side sits the mutual fund — regulated, accessible, but restricted to long-only strategies. On the other is PMS, with meaningful flexibility but a ₹50 lakh entry barrier that shuts out most serious investors who want something more sophisticated without committing that kind of capital upfront.

SIFs sit between the two. With a minimum investment of ₹10 lakh per PAN, they open the door to strategies that go beyond the constraints of traditional funds — long-short equity, derivative-based positioning, multi-asset allocation. The pooled structure and published NAVs feel familiar. The strategy underneath can be meaningfully different.

SEBI caps net short exposure at 25% of net assets — enough to allow genuine downside positioning in falling markets, which retail investors in regulated vehicles have never had access to before. And that matters, because markets do not always go up. Every portfolio needs a product that can work even when they don’t — and SIF is built precisely for that.

Where things stand today

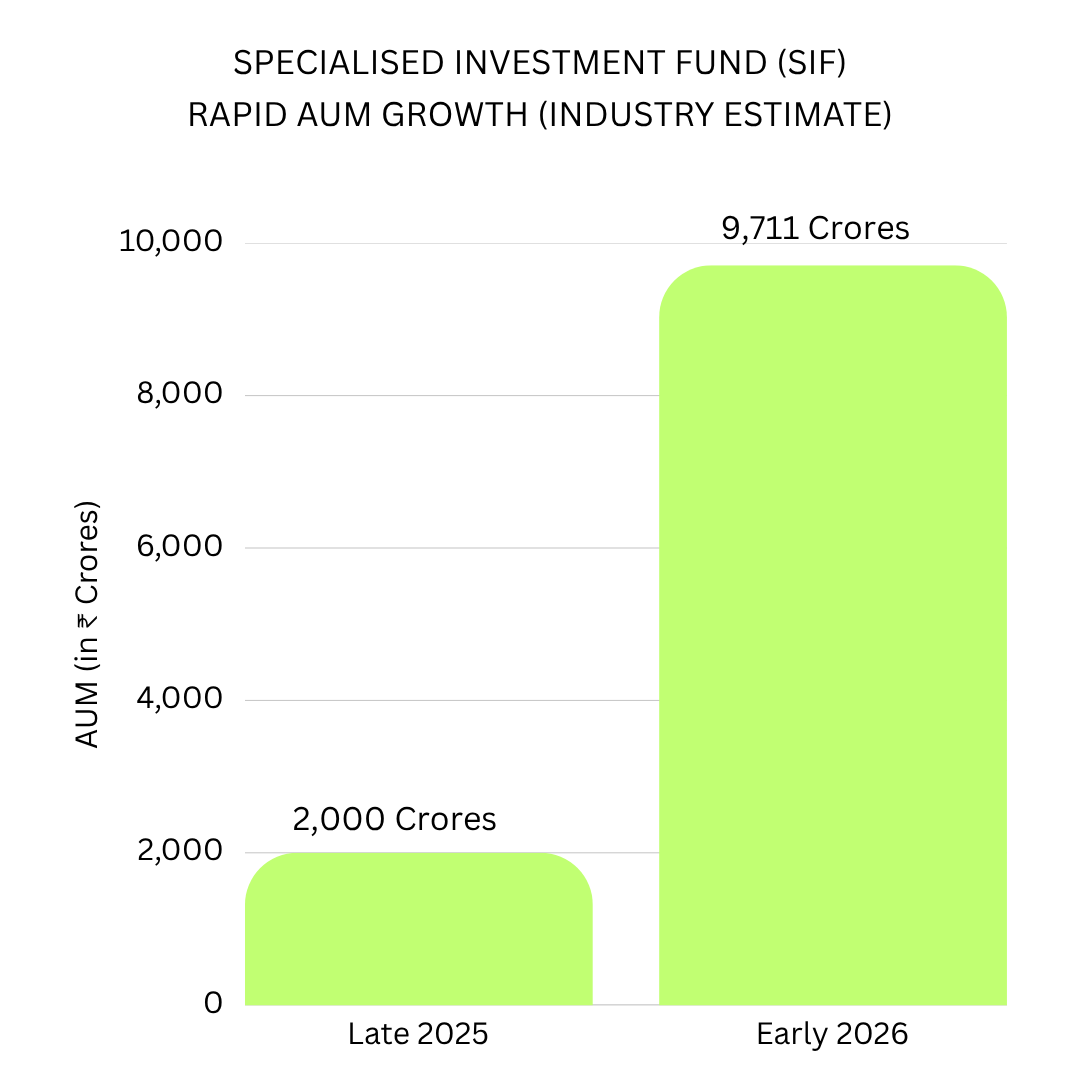

Early numbers are encouraging on the surface. As of early 2025, only 4–5 funds have been launched across major AMCs — Quant, SBI, ICICI, Tata, Edelweiss — and AUM has grown roughly five-fold since late 2025. But with so few funds and such a short track record, there is simply not enough data yet to draw firm conclusions about performance.

What we do know is that the picture is mixed. Hybrid long-short strategies, which blend equity and debt with limited derivatives, have seen the bulk of inflows and delivered modest positive returns. Pure equity long-short SIFs, meanwhile, have struggled during volatile stretches — the very conditions they were theoretically built for.

This points to a deeper issue that no regulatory framework can solve overnight: the ability to short well is genuinely rare. India’s equity markets have been built on long-only thinking for decades. Category III AIFs have had shorting permissions for years, yet most run predominantly long books in practice. SIFs inherit that same cultural starting point, and changing that mindset across an entire fund management industry takes time

The structural tension

There’s also an interesting gap in the framework itself. SEBI sets a ceiling on short exposure but no floor. A fund can legally call itself “long-short” while maintaining near-zero short positions. This creates the risk of SIF-in-name-only products — essentially mutual funds with a fancier label and a higher entry ticket. Distributors and investors will need to look beyond the category name and into actual portfolio construction before committing capital.

Will the category find its footing?

Here is where the mutual fund parallel becomes instructive. Mutual funds in their first decade were not delivering great returns, did not have trusted distributors, and had almost no investor education behind them. The infrastructure, the habits, the trust — all of it took time. No one in 1975 would have confidently predicted what mutual funds would become by 2015.

SIFs face a similar trajectory. The framework is sound. The investor gap it addresses is real. Tax treatment, in many cases, is more efficient than PMS. And the minimum ticket is low enough to build genuine scale over time.

But scale requires ecosystem maturity — fund managers who actually develop short-selling conviction, advisors who can explain these products clearly, and most critically, a full market cycle of performance data. The oldest SIF is barely a year old. Judging it now would be like writing off mutual funds in 1966.

The honest answer is that no one knows yet. But that uncertainty cuts both ways. The structural need is real, the category is live, and the players are serious. Three to five years from now, SIFs could be a standard part of sophisticated investor portfolios — or a cautionary tale about regulatory innovation outpacing market readiness

Sources: NISM (nism.ac.in), JM Financial Services, SEBI Circulars, AMFI. All figures approximate. Consult a SEBI-registered financial advisor before investing